Many merchants assume that adding new payment methods means rebuilding their website, marketplace or checkout. In most cases, it doesn’t. If your website, app or platform already sells, a payment gateway for existing websites can add card, crypto, stablecoin and alternative payment options to the setup you already run — without migrating platforms or starting again.

Merchants running WooCommerce, Magento, PrestaShop, a custom WordPress build or an entirely bespoke checkout often reach the same point: traffic is fine, products are fine, but payments are the bottleneck. Declined cards, missing payment methods, unclear settlement timing or high-risk restrictions can hold back a business that otherwise works. Before assuming the fix is a new store, it’s worth separating the sales channel from the payment layer sitting behind it.

What is a payment gateway for existing websites?

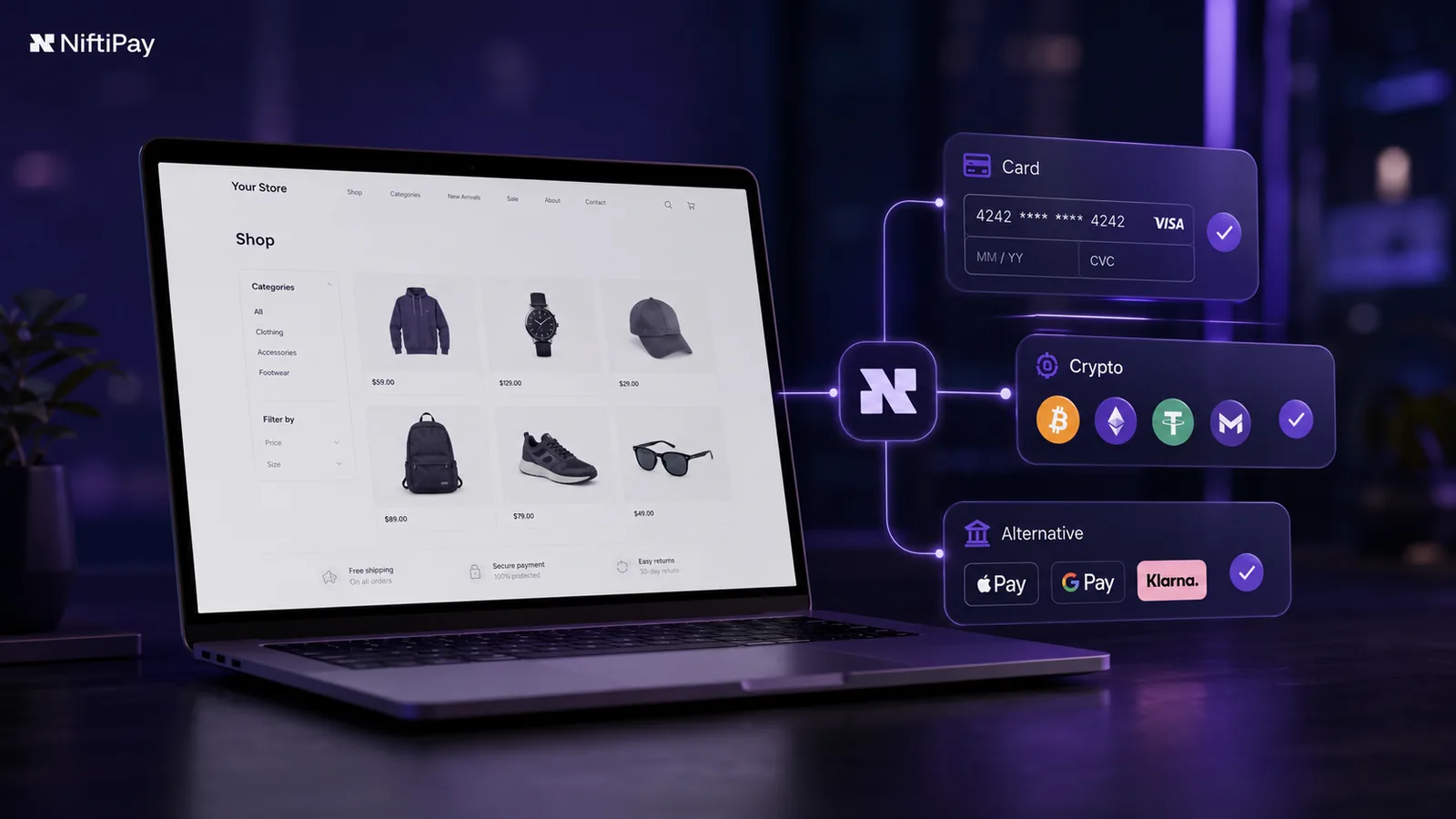

A payment gateway for existing websites is the infrastructure that connects your current sales channel — website, marketplace, app or custom platform — to payment processing, checkout, transaction status, settlement and payouts. It sits behind the storefront you already have, handling how a payment is authorised, tracked and settled, rather than replacing the storefront itself. The concept builds on the standard payment gateway model, extended to plug into commerce systems that already exist rather than requiring a new one.

Depending on your business model and the provider’s approval process, this layer can support card payments, crypto payments, stablecoins, or alternative payment methods — often side by side, through one integration rather than several disconnected providers. This is what people mean when they talk about payment infrastructure for online businesses: not a new place to sell, but a stronger way to get paid on the channel you already have.

When your current sales channel works but payments create friction

A working website and a working payment setup are not always the same thing. It’s common for a store, marketplace or platform to generate real traffic and orders while the payment layer quietly holds it back. Typical friction points include:

- Failed or declined payments that have nothing to do with product demand

- Limited payment method coverage — no crypto, no local alternative methods, no options for international buyers

- High-risk merchant restrictions that block acceptance for certain categories or business models

- Poor checkout clarity, where customers aren’t sure whether a payment went through

- Slow or unclear settlement, making it hard to plan cash flow

- Fragmented payout processes across multiple providers or currencies

- Customer confusion after payment, which drives support tickets and disputes

In practice, these frictions show up as abandoned carts, support tickets asking whether a payment actually went through, and finance teams reconciling payouts by hand at the end of every month. None of these problems are solved by moving to a new platform. They live in the payment infrastructure, not the storefront — which is why rebuilding rarely fixes them.

Why merchants may need card, crypto and alternative payment methods

For most online businesses, one payment method is no longer enough. Customer preference varies by market, buyer demographic and product category, and international buyers in particular often expect options beyond a standard card form.

A card and crypto payment gateway gives merchants a way to accept traditional card payments alongside crypto and stablecoin payments, which can be useful for cross-border trade, digital goods, or customers who prefer not to rely on card rails. An alternative payment gateway extends this further with local or non-card methods relevant to specific regions or customer bases.

In practice, this often means stablecoins such as USDT or USDC for cross-border settlement, alongside locally relevant alternative methods — bank transfers, open banking payments or buy-now-pay-later options — depending on the markets a merchant sells into. No single combination suits every business; the right mix depends on where customers are and how they prefer to pay.

This matters most for merchants in restricted categories, where standard acquirers are cautious, or businesses managing risk across multiple markets. Adding payment flexibility does not guarantee higher approval rates or conversion — it depends on underwriting, business model and market fit — but it does widen the range of customers a business can serve without depending on a single processor.

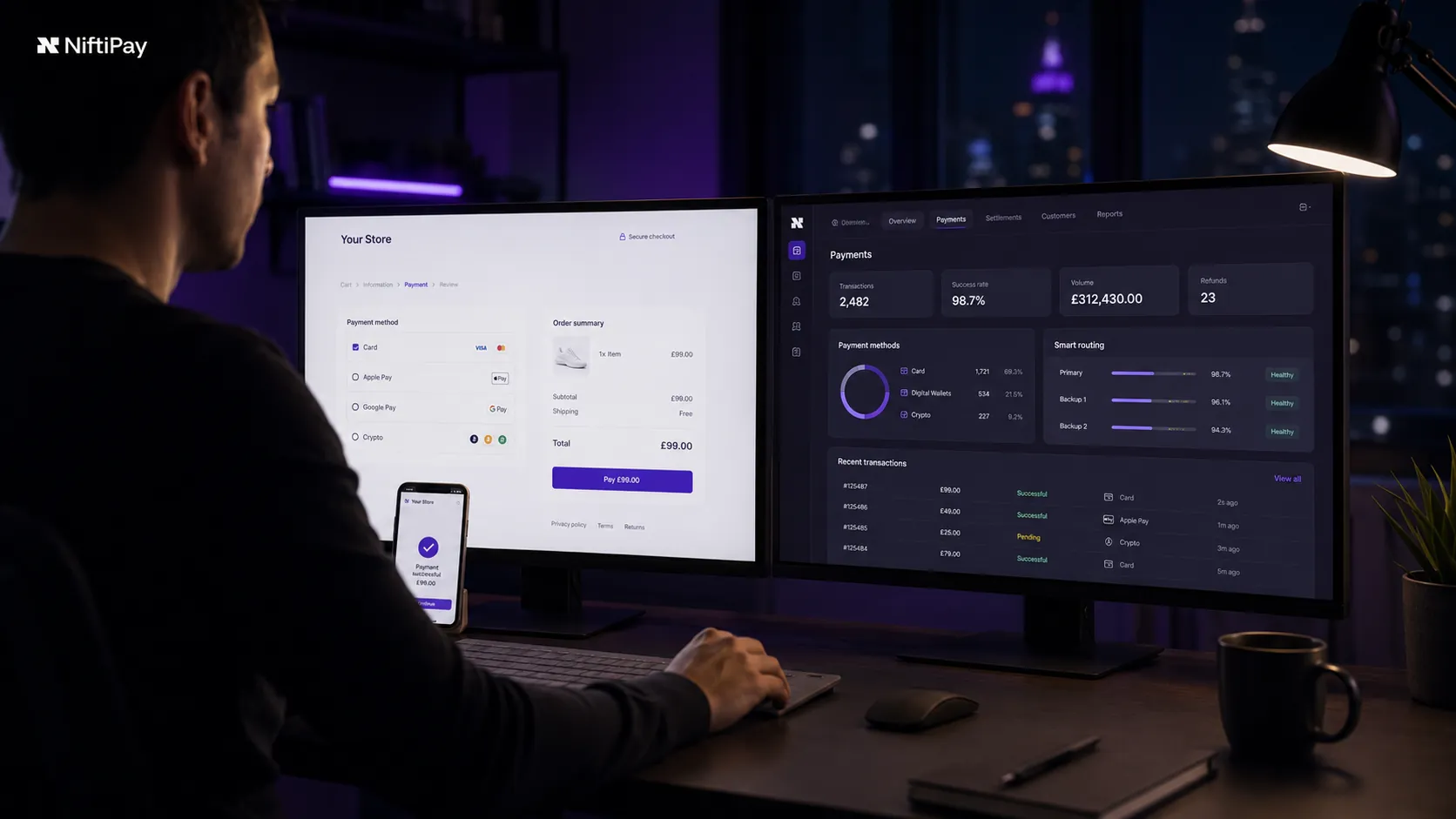

How checkout, settlement and payout fit together

A payment gateway is not just the “pay now” button. It affects a full lifecycle that runs well beyond the checkout page:

- Checkout — the customer submits payment details through your existing storefront

- Authorisation or confirmation — the payment method, card network, or crypto network confirms the transaction can proceed

- Transaction status — the payment is marked pending, approved, failed or settled, and that status needs to be visible to the merchant and, where relevant, the customer

- Settlement — funds move from the payment method into the merchant’s available balance, on a timeline that varies by method and provider

- Payout — settled funds are paid out to the merchant’s bank account, wallet, or nominated destination

For example, a WooCommerce store accepting both card and stablecoin payments needs one settlement report that reconciles both — not two disconnected dashboards that finance has to match by hand at month end.

Clear transaction status and payment visibility matters more than it might seem. Support teams need it to answer customer questions, finance teams need it to reconcile accounts, and operations teams need it to catch problems before they become disputes. A well-structured checkout-to-settlement flow is often the difference between a payment setup that scales and one that generates ongoing support overhead.

What to check before adding a new payment gateway

Before switching or adding a payment gateway, it helps to work through a practical checklist rather than comparing providers on price alone. Compliance expectations are worth checking early, too — most providers require alignment with PCI DSS standards before any card data can be processed:

- Current platform or sales channel — WooCommerce, Magento, PrestaShop, custom WordPress, app or bespoke checkout, and how the gateway connects to it

- Payment methods needed — cards, crypto, stablecoins, or specific alternative methods for your customer base

- Supported currencies — both for acceptance and for settlement/payout

- High-risk or restricted business model considerations — whether your category needs specialist underwriting

- Checkout integration requirements — hosted page, embedded fields, or full API control

- API or plugin needs — whether your team can integrate directly or needs a ready-made plugin

- Settlement and payout expectations — timing, currency, and reporting clarity

- Documentation, onboarding, KYC/KYB and compliance requirements — what information the provider needs before you can go live

- Customer support and transaction visibility — how disputes, refunds and failed payments are handled day to day

Providers that publish clear security and access controls and a documented API integration path are generally easier to evaluate than those that only disclose pricing after a sales call.

When to use Niftipay instead of rebuilding your commerce setup

Niftipay is designed for merchants who already have a functioning website, marketplace, app or platform, where the main issue is payments, checkout or settlement rather than the storefront itself. It may be a better fit than a full rebuild when:

- Your sales channel already converts, but payment acceptance, approval rates or settlement timing are holding growth back

- You need card, crypto, stablecoin or alternative payment methods added to an existing checkout rather than a new one built from scratch

- Your business model sits in a high-risk or complex category and needs a payment layer built with that in mind

- You want a payment infrastructure partner that can work alongside your current systems rather than replace them

- You’d rather avoid the cost, downtime and risk of an unnecessary platform migration

Niftipay can help merchants in these situations connect card, crypto and stablecoin payment infrastructure to what they’ve already built. It is designed as a payment layer, not a website or store builder — the goal is to strengthen the infrastructure behind your existing sales channel, not to give you a new one.

What actually changes when you add payment infrastructure instead of rebuilding?

It helps to see the payment layer as separate from the storefront layer. Here’s what each part of a payment gateway for existing websites is responsible for:

| Layer | What it does | Why it matters |

|---|---|---|

| Checkout integration | Connects your existing storefront to payment processing without changing the customer-facing experience | Avoids the cost and risk of migrating platforms |

| Card acceptance | Processes traditional card payments through standard rails | Covers the majority of everyday transactions |

| Crypto and stablecoin acceptance | Accepts crypto or stablecoin payments alongside cards, where approved | Serves customers and markets that cards don’t reach well |

| Settlement | Moves authorised funds into the merchant’s available balance | Determines how quickly revenue becomes usable cash |

| Payout | Transfers settled funds to the merchant’s bank or wallet | Affects cash flow planning and reconciliation |

| Onboarding and compliance | Verifies the business through KYC/KYB before go-live | Determines which payment methods and limits are available |

FAQs

Can I add a payment gateway to an existing website?

Yes. In most cases you don’t need to migrate platforms or rebuild your storefront. A payment gateway for existing websites connects to your current checkout — whether that’s WooCommerce, Magento, PrestaShop, a custom WordPress build or a bespoke platform — and handles authorisation, transaction status, settlement and payouts behind it.

Do I need to rebuild my store to accept crypto payments?

No. Crypto and stablecoin acceptance is typically added as an additional payment method within your existing checkout, not as a reason to change platforms. The integration point is the payment layer, not the storefront.

Can one gateway support card and crypto payments?

Some payment infrastructure providers, Niftipay included, are built to support card, crypto and stablecoin payments through a single integration, depending on the merchant’s business model and approval. This can reduce the number of separate providers a business needs to manage, though the exact methods available will depend on underwriting and the markets the business serves.

What should merchants check before changing payment gateway?

At minimum: which payment methods and currencies you need, whether your business model falls into a restricted or high-risk category, what your current platform requires for integration, how settlement and payouts are structured, and what documentation, KYC/KYB or PCI DSS alignment the provider requires during onboarding.

Is Niftipay suitable for merchants with an existing sales channel?

Niftipay is designed for merchants who already have a working website, marketplace, app or platform and need stronger payment infrastructure — card, crypto, stablecoin or alternative payment methods — rather than a new place to sell. It is not a website or store builder.

Most merchants who reach out about “switching payment providers” don’t actually need a new store — they need their existing one to stop being held back by the payment layer behind it. Worth checking which one you actually have before you rebuild anything.