Your WooCommerce store may already be doing everything right. The catalogue is solid, orders are coming in, customers are returning — but payments keep causing friction. If applications get declined, payout dates slip, or card acceptance feels more limited than it should be, the problem usually isn’t WooCommerce itself. It’s whether the high-risk WooCommerce payment gateway behind your checkout can actually support your business model.

This article isn’t about migrating platforms or rebuilding your store. It’s about understanding what “high-risk” means in payments, what providers check before approval, and how to prepare properly — whether you stay with your current setup or look at alternatives like Niftipay.

Why some WooCommerce businesses are considered high-risk

“High-risk” is a payments industry classification, not a judgement on the legitimacy of your business. It simply means a provider needs more documentation, more monitoring or tighter controls before it will process your transactions. A well-run store can still fall into this category.

Common reasons a WooCommerce store gets classified as high-risk:

- Business category or product type — sectors such as supplements, adult content, gaming, travel, coaching or digital products are flagged more often by card networks.

- Chargeback exposure — industries with naturally higher dispute rates draw closer scrutiny.

- Refund history — a pattern of refunds can signal product, fulfilment or expectation-setting issues to a processor.

- Cross-border sales — selling into multiple countries adds currency, tax and fraud-pattern complexity.

- Subscription or recurring billing — recurring charges carry a higher chargeback and dispute profile than one-off purchases.

- High average order value — larger transactions represent more exposure per dispute.

- Regulated or restricted sectors — anything touching financial services, health claims, or age-restricted goods invites extra checks.

- Crypto or alternative payment needs — wanting to accept digital assets alongside cards narrows the pool of providers willing to work with you.

- Fulfilment or delivery risk — pre-orders, long shipping times or dropshipping models increase dispute likelihood.

- Previous merchant account issues — a prior termination or rolling reserve elsewhere follows a business into future applications.

None of this means a WooCommerce merchant account is impossible to get. It means the provider needs a clearer picture of the business before taking on the risk — often through a high-risk WooCommerce payment gateway built specifically for that profile, rather than a standard one stretched to fit.

Payment issues WooCommerce merchants often face

When a mainstream gateway isn’t built for a merchant’s risk profile, the problems tend to show up gradually rather than all at once. Some of the most common issues:

- Declined applications, sometimes with little explanation

- Sudden account reviews after a spike in volume or a change in product mix

- Payment holds on individual transactions

- Rolling reserves that tie up a percentage of revenue for weeks or months

- Limited card acceptance, particularly for international cards

- No option to accept crypto or stablecoin payments

- Poor checkout flexibility — one processor, one flow, no fallback

- Unclear payment status, making it hard to know what’s actually been settled

- Slow settlement times

- Payout delays that disrupt cash flow planning

- Chargeback management that feels reactive rather than structured

- Customers abandoning checkout because their preferred payment method isn’t available

That last point matters more than it’s often given credit for. Every unsupported payment method at checkout is a customer decision point, and for high-risk categories where trust is already a factor, checkout friction compounds quickly. We’ve covered this in more detail in our piece on reducing checkout friction for high-risk stores without loosening fraud controls.

What payment providers check before approval

Whether you’re applying with a mainstream acquirer or a specialist WooCommerce high-risk payment processor, the underwriting process looks at broadly the same things. Knowing this in advance saves time and avoids a rejected application that then makes the next application harder.

Providers typically review:

- Business registration details and legal entity structure

- Ownership information for directors and beneficial owners

- Website and product transparency — can a reviewer tell exactly what you sell?

- Refund and shipping policies, and whether they’re actually published

- Terms and conditions covering the sales process

- Chargeback history from any previous processor

- Processing volume, both current and projected

- Average transaction value

- Countries served and where customers are based

- Fulfilment model — in-house, dropshipping, third-party logistics

- Customer support process and response times

- Compliance documentation relevant to your sector

- Risk category and how it’s been assessed previously

- Expected payment methods, including card, crypto or bank transfer

- Settlement and payout expectations, including currency and frequency

This is also where WooCommerce payment gateway approval most often stalls — not because the business is unacceptable, but because documentation is incomplete or the website doesn’t clearly reflect what’s being sold. Providers also look closely at security posture; our overview of payment gateway security controls covers the access, authentication and withdrawal protections that reviewers expect to see in place.

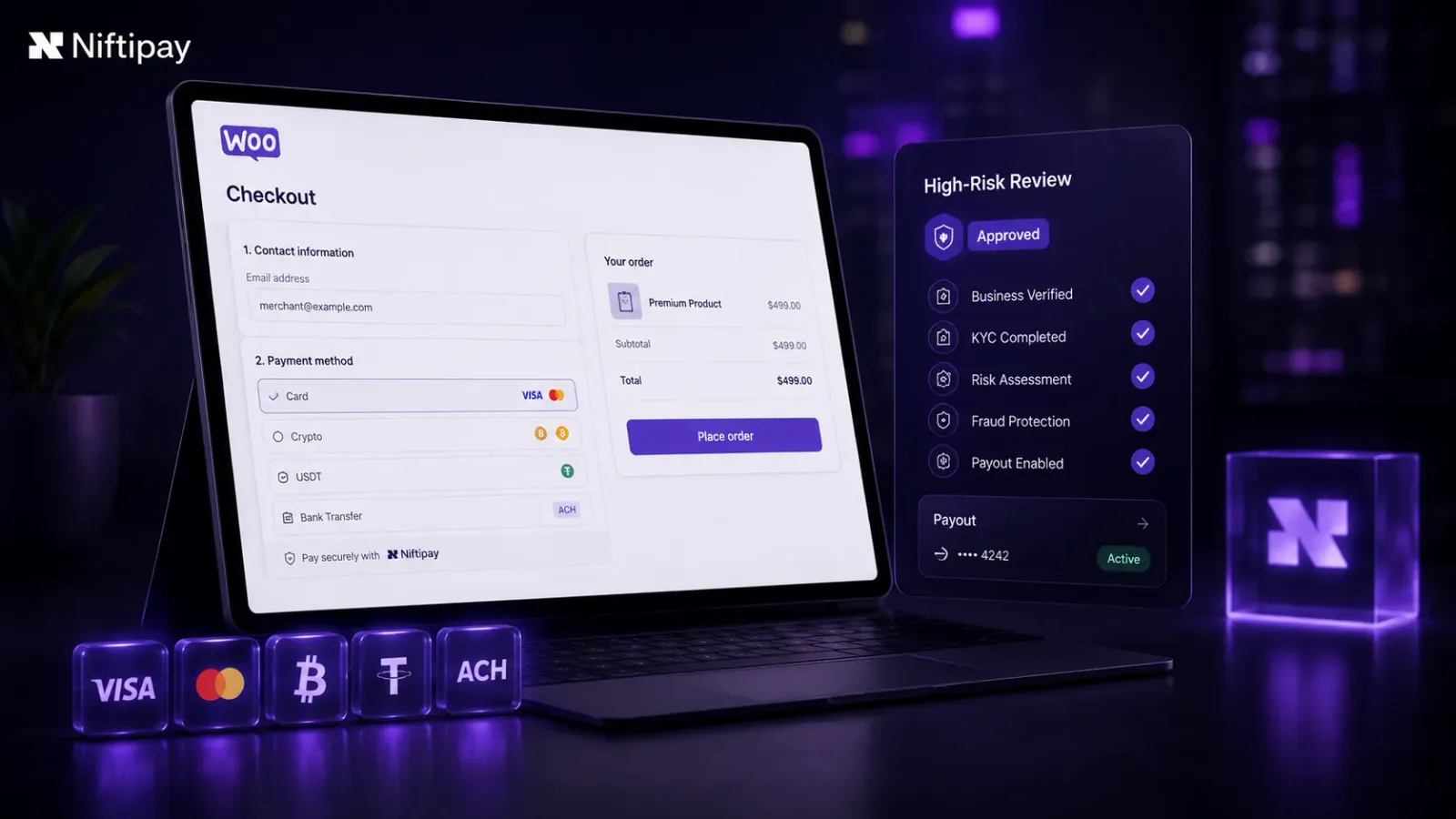

Card, crypto and alternative payment options for WooCommerce

Most WooCommerce merchants still need card payments as the primary rail — it’s what most customers expect and use by default. But relying on a single card processor leaves a store exposed if that processor tightens its risk appetite, adds a reserve, or simply doesn’t renew.

This is where payment diversity becomes practical rather than optional:

- Card payments cover mainstream customer behaviour and remain the default expectation at checkout.

- WooCommerce crypto payments give customers who prefer digital assets a route to pay without needing a card at all — useful for merchants serving international audiences or crypto-native customer bases.

- Stablecoin payments can simplify certain cross-border or higher-complexity flows, since the settlement value doesn’t move with market volatility the way other digital assets do.

- Alternative payment gateways act as a backup layer, so a single provider’s decision doesn’t take the whole checkout down.

Adding these options doesn’t remove risk or guarantee approval elsewhere — a crypto option sits alongside card processing, not instead of proper underwriting. What it does is reduce dependency on any one provider, which matters for merchants who’ve already experienced a hold, a reserve or a sudden review. Our guide on combining card and crypto in a single payment gateway looks at when that consolidation makes sense, and our piece on crypto payment processing and vendor settlement goes deeper into how digital asset settlement actually works in practice.

Settlement and payout considerations

Choosing a payment gateway isn’t only about what happens at checkout. What happens after a payment is authorised — how it moves towards settlement and eventually reaches your bank account — has a direct effect on cash flow.

Things worth understanding before you apply:

- How an authorised payment actually moves towards settlement, and what can delay it

- Payout timing — daily, weekly or on a rolling schedule

- Payout currency, and whether conversion happens automatically

- Reserve requirements, including whether they’re a fixed amount or a rolling percentage

- Settlement reporting — can you actually reconcile what you’re paid against what you sold?

- Transaction visibility while a payment is still moving through the system

- Reconciliation workload for your finance team or bookkeeper

Payout uncertainty is one of the most underestimated risks in a high-risk setup. A merchant can have healthy sales and still run into cash flow strain if reserves are unclear or settlement takes longer than expected. We’ve mapped out exactly how this works in our breakdown of the checkout-to-settlement-to-payout flow, and our piece on tracking payment status explains how to get visibility on pending, approved and settled transactions rather than guessing. Before applying anywhere, ask directly about fees, reserve terms and payout schedules — these details are often easier to negotiate before signing than after.

How to prepare before applying for a high-risk WooCommerce payment gateway

Preparation is what separates a fast approval from a rejected application and a harder second attempt. Most of this work happens on your store and in your documentation, not with the provider.

Before applying for a high-risk payment setup for WooCommerce merchants, work through this checklist:

- Make sure product pages are transparent — clear descriptions, pricing and what the customer is actually buying

- Publish clear refund, shipping and terms pages, and link to them from checkout

- Prepare company documents: registration, ownership structure, proof of address

- Understand your expected monthly volume, realistically rather than optimistically

- Document fulfilment timelines so a reviewer can see how orders are actually delivered

- Review your chargeback history and be ready to explain any spikes

- Identify which payment methods you actually need — card, crypto, bank transfer or a mix

- Clarify which countries and currencies you sell into

- Decide whether card, crypto or alternative payments are needed now or likely needed soon

- Prepare for KYC and KYB checks — identity verification for individuals and the business itself

- Be honest about your business model and risk category from the outset

That last point is worth emphasising. Providers can usually work with a clearly explained high-risk business. What they can’t work with is a business that undersells its own risk profile during onboarding and then triggers a review once the discrepancy shows up in live transaction data.

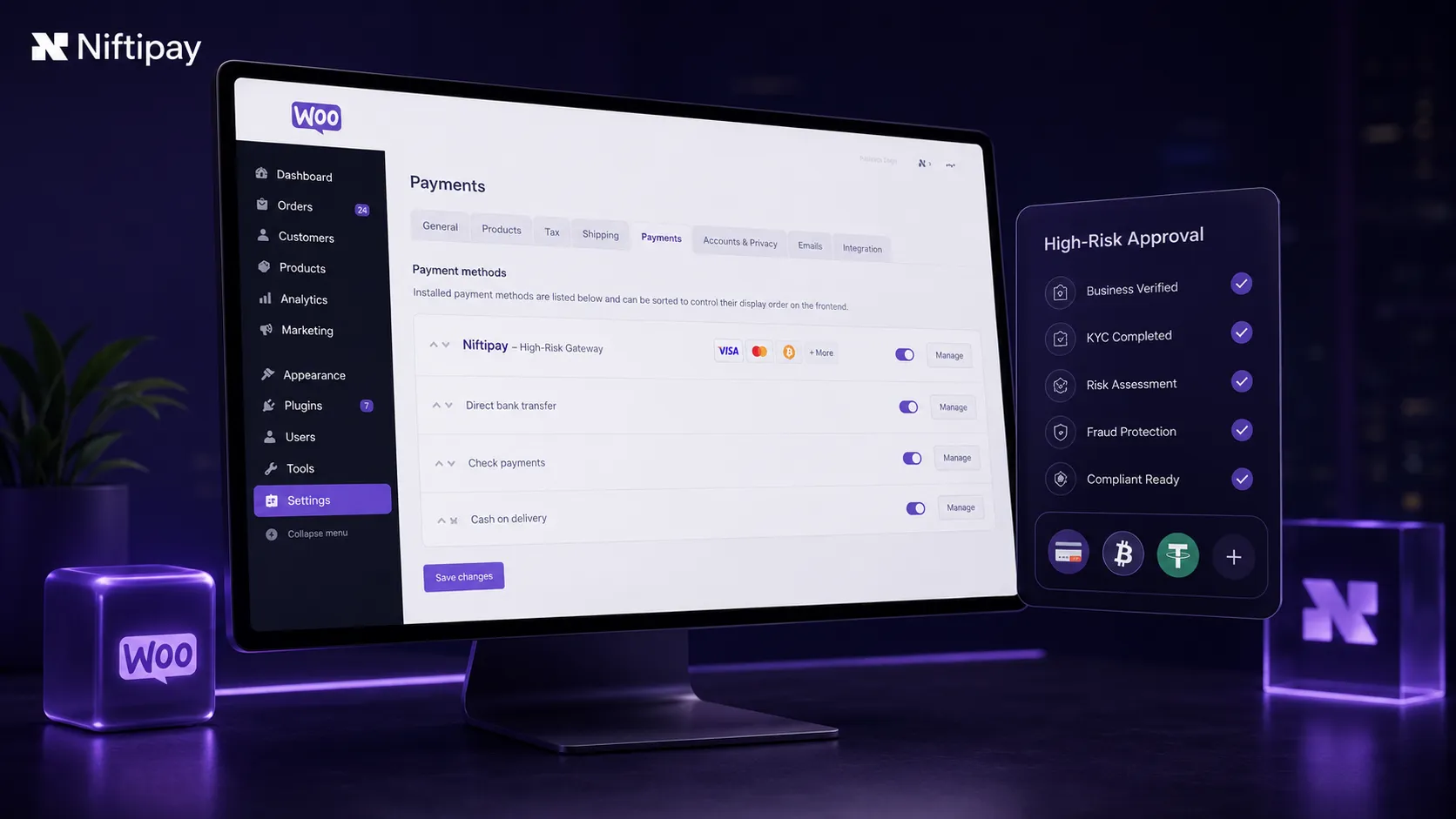

When Niftipay may be a better fit for WooCommerce merchants

Niftipay is not a store builder or an ecommerce platform. It’s a payment infrastructure layer designed to sit behind a store that already works — including WooCommerce — and handle card, crypto, stablecoin and alternative payment acceptance.

Niftipay may be a suitable WooCommerce payment gateway for high-risk merchants when:

- The store already has products, content, orders and customers in place

- The main issue is payment acceptance, not the ecommerce platform itself

- The merchant needs card, crypto, stablecoin or alternative payment options in one setup

- The merchant wants to avoid rebuilding or migrating their store just to fix a payments problem

- Clearer settlement and payout infrastructure would materially help with cash flow planning

- The business operates in a complex or high-risk category that needs more structured underwriting

- The merchant is preparing to apply and wants to understand approval requirements properly first

Support here is subject to qualification, and fit depends on the merchant’s business model, risk profile and approval requirements — this isn’t a guarantee of approval, and no provider should promise one. What Niftipay can support is a WooCommerce merchant who already has a working sales channel and needs the payment layer behind it to catch up. For merchants specifically looking to add payment options to a store that already works, our guide on adding a payment gateway to an existing website without rebuilding it covers that process in more detail.

Is a WooCommerce high-risk payment gateway right for your store?

Use this as a quick reference before deciding whether to apply, switch providers, or add a secondary payment layer.

| Signal you’re seeing | What it usually means | What to check before applying |

|---|---|---|

| Application declined with little explanation | Documentation or risk category unclear to the provider | Business registration, ownership info, website transparency |

| Rolling reserve applied | Provider managing chargeback or fraud exposure | Reserve percentage, release schedule, alternatives |

| No crypto or stablecoin option | Current gateway doesn’t support digital assets | Whether WooCommerce crypto payments are actually needed |

| Payout dates inconsistent | Settlement or reporting process lacks visibility | Payout currency, frequency and reconciliation reporting |

| Checkout abandonment rising | Limited payment methods at checkout | Card, crypto and alternative gateway coverage |

| Sudden account review | Volume, product mix or dispute rate changed | Chargeback history, current processing volume |

FAQs

What is a high-risk payment gateway for WooCommerce?

A high-risk payment gateway for WooCommerce is a payment processing setup built for merchants whose business category, transaction pattern or risk profile requires closer underwriting than a standard gateway offers.

It typically involves more documentation at onboarding, ongoing monitoring, and sometimes reserve arrangements — in exchange for approval and support that mainstream providers may not offer to the same business.

Why would a WooCommerce store be considered high-risk?

A store can be classified as high-risk for several reasons, including its product category, chargeback history, refund patterns, cross-border sales, subscription billing, or a previous merchant account issue.

It’s a risk classification used by processors, not a comment on whether the business is legitimate. Many well-established WooCommerce stores operate long-term with a high-risk payment setup.

Can WooCommerce merchants accept crypto payments?

Yes. WooCommerce crypto payments can be added alongside card processing through the right payment infrastructure, giving customers who prefer digital assets an option at checkout without removing card acceptance for everyone else.

Stablecoins are often used for this because their value doesn’t fluctuate the way other digital assets do, which makes settlement more predictable for the merchant.

What do providers check before WooCommerce payment gateway approval?

Providers generally review business registration and ownership details, website and product transparency, refund and shipping policies, chargeback history, processing volume, average transaction value, countries served, and expected payment methods.

They also want clarity on fulfilment model and settlement expectations. Merchants who prepare this documentation in advance tend to move through approval faster than those who apply reactively.

Do I need to rebuild my WooCommerce store to use Niftipay?

No. Niftipay is designed to work as a payment infrastructure layer behind a store that already exists — it isn’t a store builder and doesn’t require migrating your catalogue, content or customer data.

If WooCommerce already works for your products and operations, the integration is about connecting stronger payment infrastructure to your existing checkout, not replacing what already works.

A WooCommerce store that already has customers, orders and a working catalogue doesn’t need to be rebuilt because a payment provider said no. More often, it needs a payment infrastructure layer that was actually built for its risk profile. Whether that means preparing a stronger application, adding a second payment method, or moving to a high-risk WooCommerce payment gateway designed for exactly this situation, the fix usually sits behind the checkout — not in the storefront itself.